What are notes to financial statements in Mexico?

Notes to financial statements are an integral part of an entity's financial statements. Their main purpose is to provide additional explanations and details that complement and clarify the information presented in the financial statements...

What are NIFs and why are they important?

The Financial Reporting Standards (NIF) are a set of technical regulations that establish how entities must prepare and present their financial information in Mexico. These standards seek to ensure that the information is comparable, relevant, reliable and...

Update of the A series of the NIF 2024

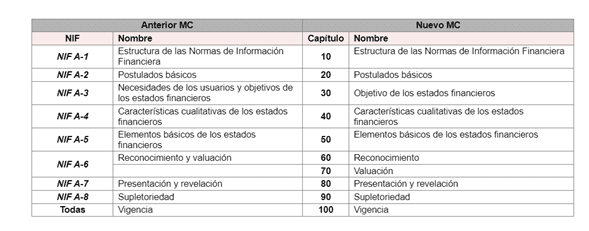

The NIFs are mainly divided into two large groups of regulatory pronouncements: the Conceptual Framework (CM) and the specific NIFs. In this article we will analyze the main differences in the CM with respect to previous years. Why is this different?

New NIF Series A Conceptual Framework (2024)

The objective of the NIF Series A is to define and establish the Conceptual Framework that supports the specific NIFs and the solution to problems that arise in the accounting recognition of transactions and any event that economically affects the...